Yes. If you or someone you know is experiencing foreclosure, you can make a new home purchase after waiting a certain period and ensuring your finances are airtight. You should not feel guilt or shame associated with the hardship but take the opportunity to find the right home. This article will cover what to expect from the process, the estimated foreclosure waiting period, and how to make a good impression on lenders.

Considerations

The first step in the process is to think carefully about the responsibility of homeownership. Asking the following questions may help:

- Am I prepared to pay for the costs of a mortgage, maintenance, insurance, and taxes?

- How much space do I need and what does the market look like today?

- When was the last time I checked my credit score?

- Have I written down a target savings goal, and how close am I to achieving it?

- How much longer do I need to wait before I start looking at homes?

- Who else will be living with me and what are their needs?

Homebuyers buying after foreclosure can expect to pay higher interest rates and down payments than on their initial permanent residences.

Financial Readiness

The financial profile for homebuyers exiting foreclosure is similar to that of a standard homebuyer, just with a more conservative approach.

Establish an Emergency Fund

Before shopping for homes, buyers should set aside a strong emergency fund that will cover their expenses for six to eight months. Buyers should anticipate unforeseen events, such as a job loss or an accident requiring medical care. One of the easiest ways to boost savings over time is to set up an automatic savings plan. Keeping the funds in a savings account separate from checking curbs the temptation to spend it.

Save Up for a Sizable Down Payment

Lenders would like to see significant down payments of at least 10-20% of the home’s sale. Remember that making a down payment of 20% or more means avoiding having to pay private mortgage insurance (PMI).

Check and Fix Credit

Credit scores and credit reports are very important when making big house moves. Buyers can check their credit scores for free once per year with the three major credit bureaus: TransUnion, Equifax, and Experian. Freezing credit is an excellent way to protect against identity theft and ensure others aren’t opening up fraudulent accounts.

It’s important to fix any errors well before applying for a mortgage loan. Keeping credit utilization at 30% or lower and debt-to-income ratio at 43% or lower is good—lower is best for credit score health. Paying down any existing debt, like a student loan or a car payment can boost credit scores.

Lending Options

Homebuyers will be offered standard options for lending with some modifications.

Loan Types

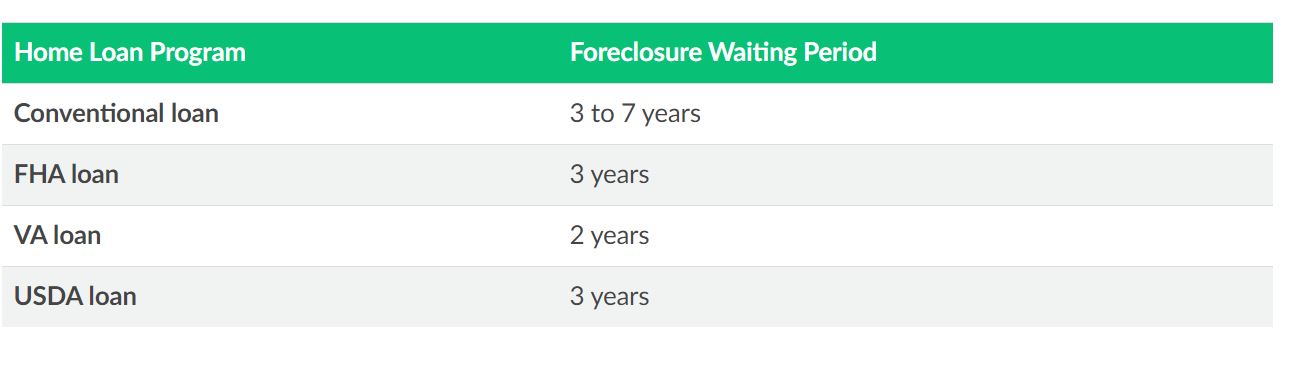

Homebuyers have several options for loans, including conventional, FHA, VA, and USDA. The linked article explains the overview and minimum requirements for each type of loan.

Foreclosure Waiting Period

Source: LendingTree

Each loan type has a different foreclosure waiting period, with the waiting period starting on the first day of foreclosure.

Extenuating Circumstances

Sometimes life events are out of buyers’ control, and if they have documented proof of a long-term reduction of income, their waiting period can be shortened. Some examples of extenuating circumstances include the death of a wage earner, job loss, and illness.

Loan Counseling

Housing counselors can provide support through The Department of Housing and Urban Development (HUD). Buyers can search for local services at HUD.gov and can receive help if they’re denied a loan after foreclosure.

The Bottom Line

The great news about buying a house after foreclosure is that you’ll have the advantage of setting high financial standards for yourself, which lenders will find favorable. Repairing your credit and demonstrating resilience will make the home buying process smoother. Remember that you can seek credit and loan counseling if you need support.